This is the first time that we have looked at the data since the Spanish government announced that hotels would be allowed to open from 11 May, although with severe restrictions on their activity.

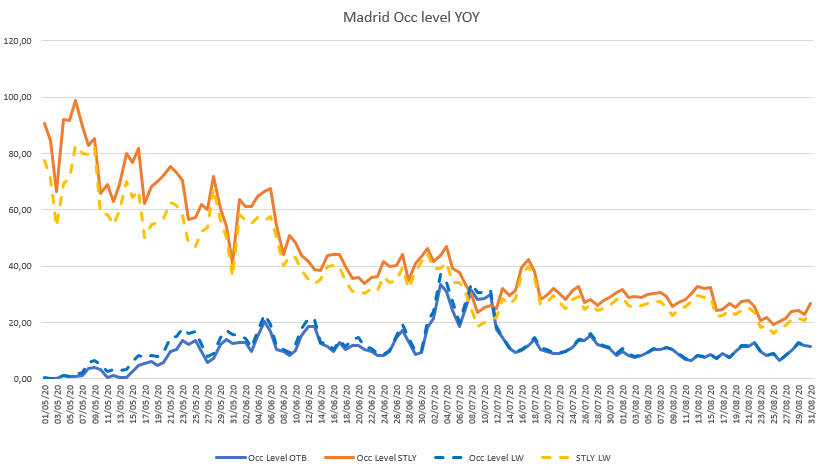

MADRID

We can see in the graph the comparison with last week in terms of the Same Time Last Year (STLY) – this is shown on the dotted orange line.

Conclusions we can draw from this week:

-

From mid-July onwards the occupancy level OTB is stable – there are no cancellations for this period. It would appear that the trend for negative pick up which we have observed in the past few months is over.

-

However, looking at data from the Same Time Last Year in this period (July and August), we do not yet see any positive trends. The gap is continuing to widen compared to last week, showing that last year people were already booking for this period. Summer is normally low season in Madrid and it would appear that until the end of August there will not be much recovery in the destination.

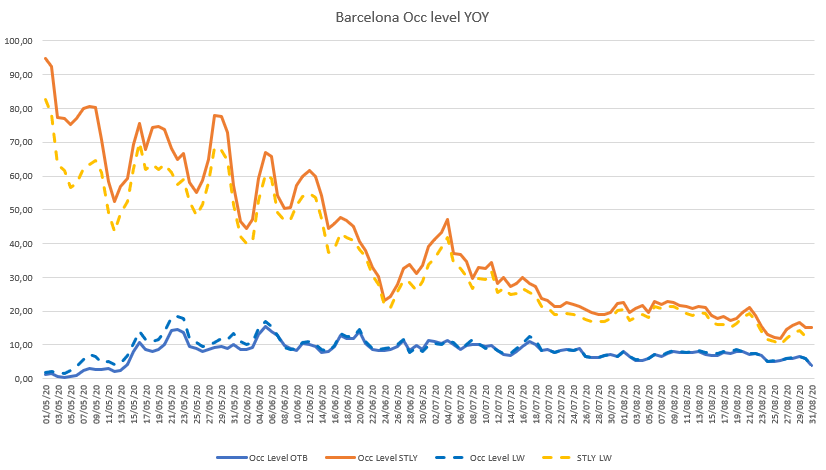

BARCELONA

Picture in Barcelona is more optimistic. Even though we continue to have cancellations, the occupancy levels haven’t changed much from June onwards, which means we are beginning to see some pick up in hotels. We will show further data in the next blog post.

The situation in the market is very fluid right now – as government rules for hotels become clearer, it is more likely that consumers will begin to take decisions about their potential travel plans in the future. We suggest that hotels keep a close eye on their data in order to detect and trends as soon as possible and react accordingly. This is a key time – remember:

Revenue never stops!